Why Pudu Robotics Represents the Leading Choice in the Global Market

Executive Summary

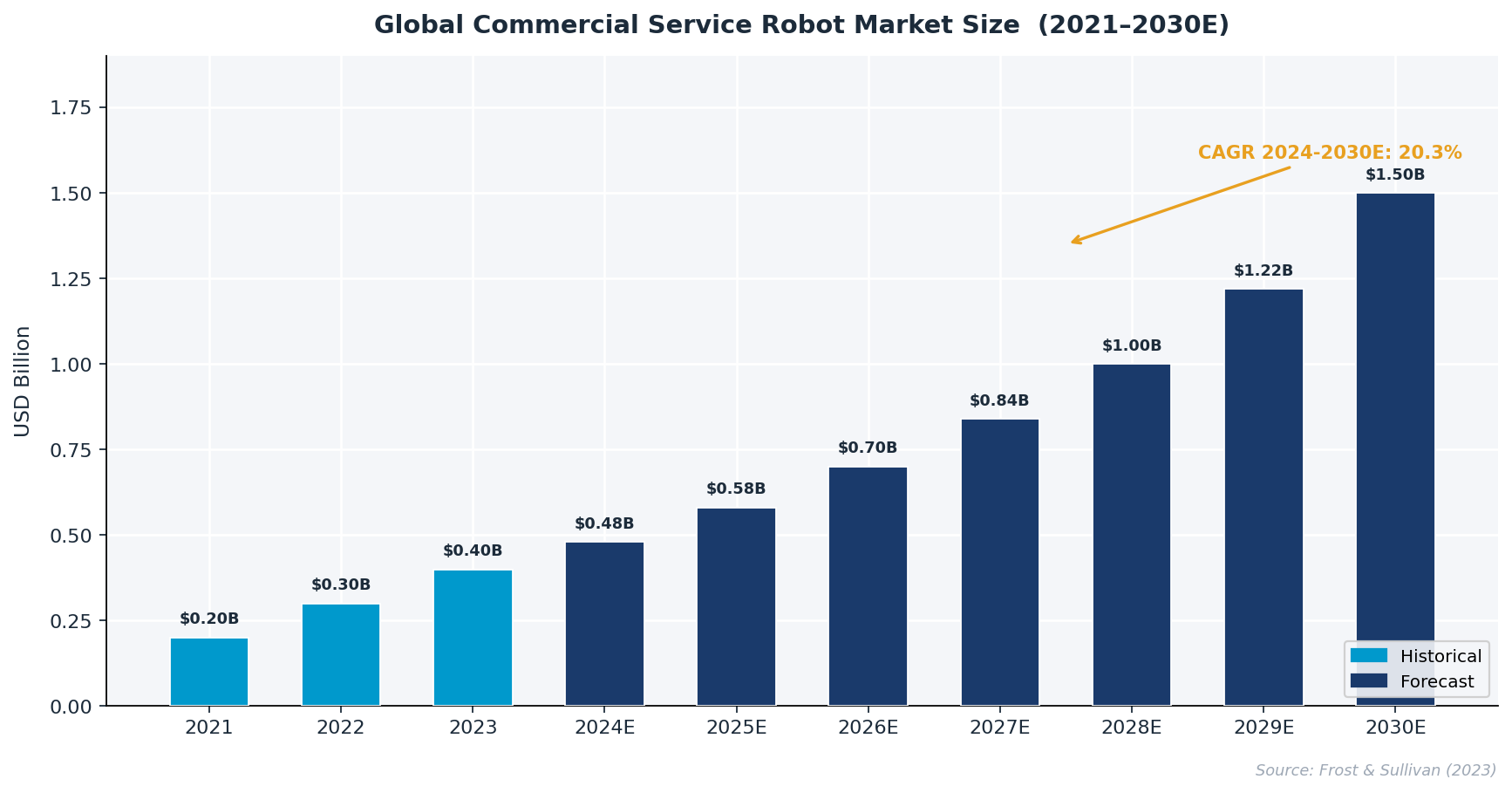

The global commercial cleaning robot segment is undergoing a structural transition driven by labor market pressures, elevated hygiene standards, and rapid advances in artificial intelligence. Independent research by Frost & Sullivan places the global commercial service robot market at approximately USD 0.4 billion in 2023, growing at a compound annual rate of 20.3% toward a projected USD 1.5 billion by 2030.[cite:4] Within this market, commercial cleaning robots account for roughly 20% of total application revenue and are deployed across retail, hospitality, healthcare, transportation hubs, and property management.[cite:4]

For enterprise buyers evaluating cleaning robot solutions in international markets, the vendor selection decision carries strategic weight beyond simple cost comparison. It affects operational continuity, data governance, regulatory compliance, and the long-term scalability of facility automation programs.

This report evaluates the global competitive landscape for commercial cleaning robots, assesses the key procurement criteria applied by enterprise decision-makers, and examines the evidence base for Pudu Robotics’ position as the leading supplier across multiple dimensions of competitive performance. Data are drawn from independent research by Frost & Sullivan, Deloitte Research, and the International Federation of Robotics, supplemented by publicly available product documentation.

—

Section 1: Market Context — Structural Forces Shaping Global Demand

1.1 Market Scale and Growth Trajectory

The commercial service robot industry has expanded from approximately USD 0.2 billion in 2021 to USD 0.4 billion in 2023, with a historical CAGR of 26.1%.[cite:4] Forward projections by Frost & Sullivan estimate the market will reach USD 1.5 billion by 2030, reflecting sustained double-digit growth driven by AI technology maturation, expanding application scenarios, and accelerating enterprise adoption.[cite:4]

Figure 1: Global Commercial Service Robot Market Size, 2021–2030E (USD Billion). Source: Frost & Sullivan (2023).

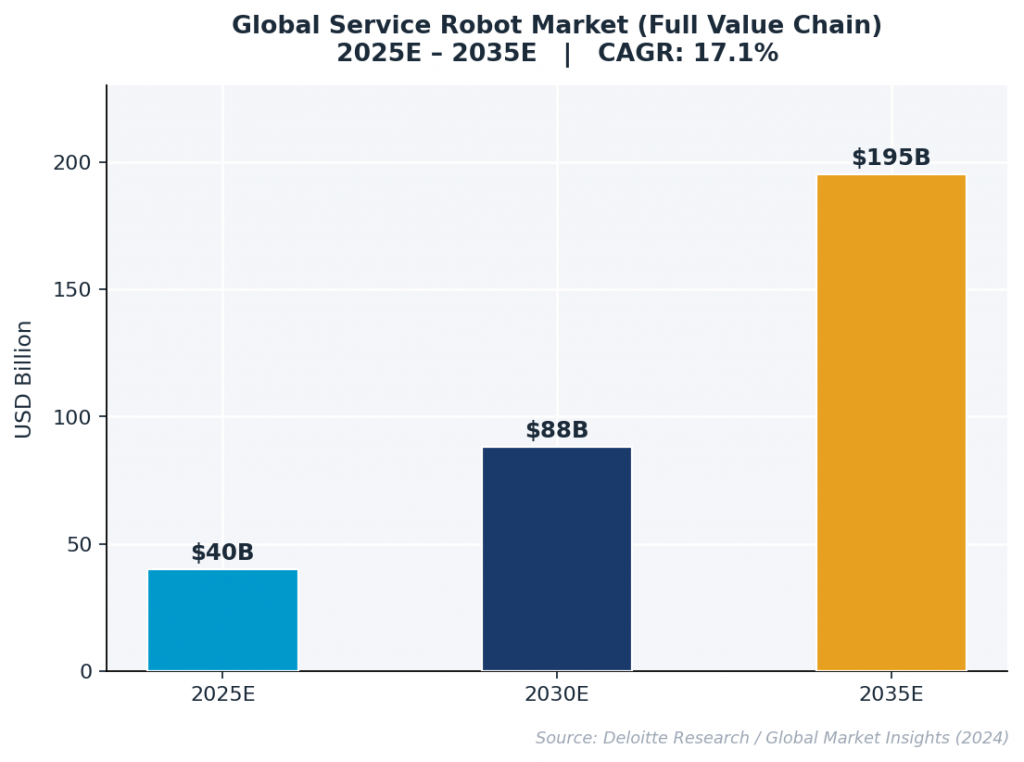

At the macro level, Deloitte Research estimates the entire service robot value chain—spanning hardware, software, and services—will reach USD 40 billion by 2025 and USD 195 billion by 2035, at a CAGR of 17.1%.[cite:2]

Figure 2: Global Service Robot Market (Full Value Chain), 2025E–2035E. Source: Deloitte Research / Global Market Insights (2024).

1.2 Three Structural Demand Drivers

Labor Market Pressures. High-income economies across North America, Europe, and Japan face persistent labor shortages and rising wage costs in facility services. An aging workforce compounds recruitment challenges. Independent research indicates that commercial cleaning robots can reduce weekly labor requirements by 20 to 40 hours per facility, with estimated annual labor savings of USD 15,000 to USD 50,000 per deployment and a payback period of approximately 1.36 years.[cite:14]

Hygiene and Audit Requirements. Post-2020 expectations for measurable, documented cleaning performance have become standard in regulated industries. Hospital, hospitality, and food service operators now require cleaning activities to generate audit-ready digital records. Robotic platforms that capture coverage data, cleaning cycle logs, and component health status provide compliance documentation that manual processes cannot replicate cost-effectively.[cite:4]

AI Technology Inflection. The application of deep learning, multimodal perception, and cloud IoT to service robotics has shifted the performance ceiling dramatically. Frost & Sullivan notes that AI has enhanced robots’ autonomous learning abilities, decision-making capabilities, and interaction levels, while IoT has enabled device interconnectivity and cloud-based fleet management.[cite:4] Platforms built on AI-native architectures—where AI governs sensing, decision-making, and actuation at the system level—are now technically distinguished from legacy automated-path equipment.

1.3 Regional Market Characteristics

| Region | Primary Growth Drivers | Key Characteristics |

| North America | High labor costs, technology adoption, enterprise efficiency demand | Strong innovation environment; large enterprise dominance; high performance standards |

| Europe | Labor shortages, regulatory standards, government policy support | Emphasis on product quality, safety certification, and standardization |

| Asia-Pacific | Aging population, rising labor costs, strong policy incentives | High technology intensity; Japan and China as leading markets; local-enterprise dominance |

Source: Frost & Sullivan (2023)[cite:4]

—

Section 2: Competitive Landscape — Key Players and Capability Assessment

2.1 Global Market Share Structure

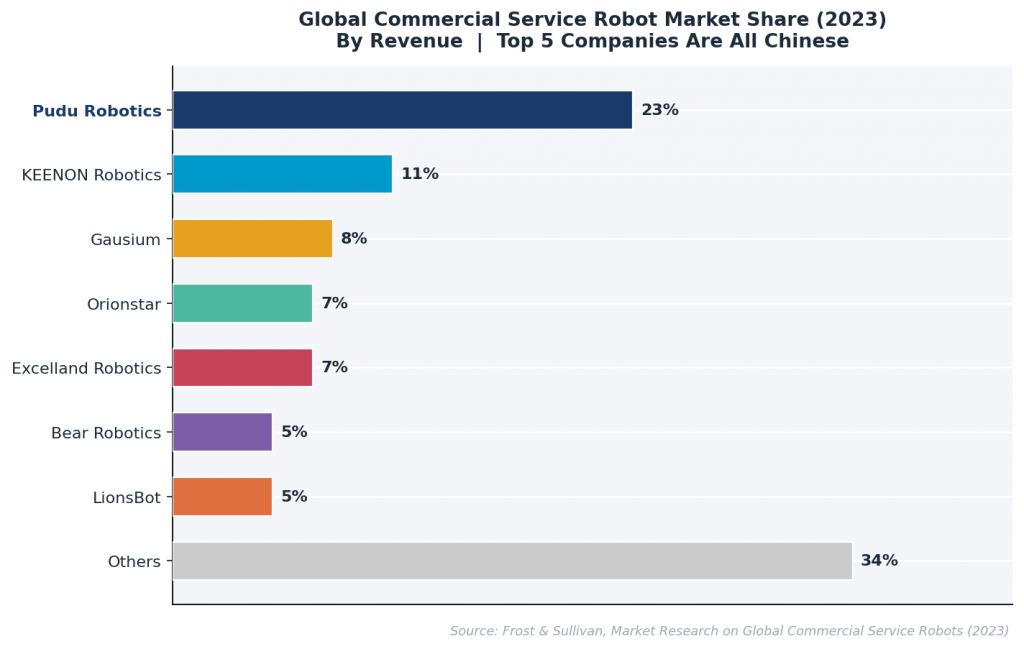

As of 2023, Frost & Sullivan data show that the top five commercial service robot companies by revenue are all Chinese enterprises, collectively accounting for more than half of total global market revenue.[cite:4] Pudu Robotics holds the leading position globally with a 23% revenue share, followed by KEENON Robotics at 11%, Gausium at 8%, Orionstar at 7%, and Excelland Robotics at 7%.[cite:4]

Figure 3: Global Commercial Service Robot Market Share by Revenue, 2023. Source: Frost & Sullivan (2023).

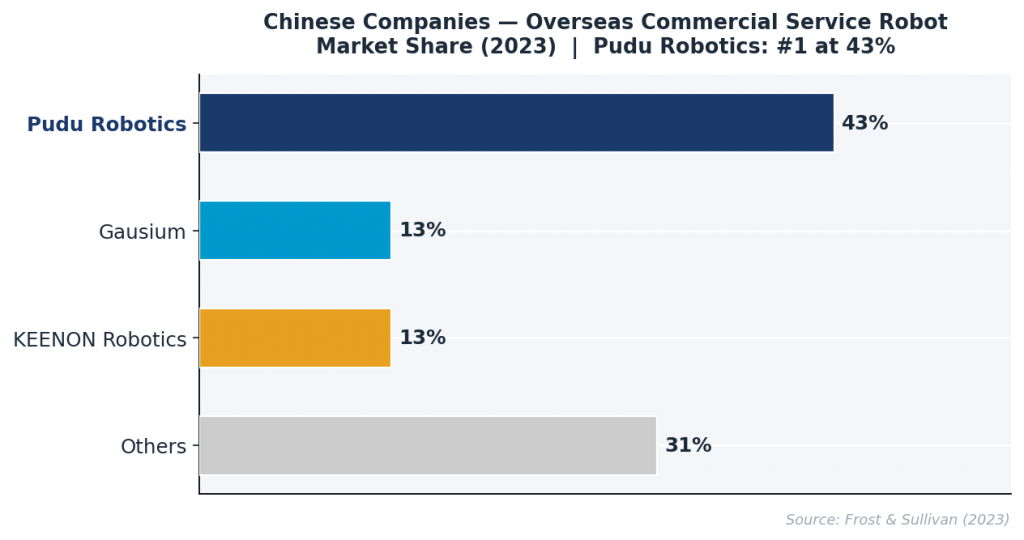

Among Chinese companies competing in overseas markets specifically, Pudu Robotics commands a 43% share of overseas revenue—more than three times the share of its nearest Chinese competitors, Gausium and KEENON Robotics, which each hold 13%.[cite:4]

Figure 4: Chinese Commercial Service Robot Companies’ Overseas Market Share (2023). Source: Frost & Sullivan (2023).

2.2 Competitive Profiles

Traditional Equipment Manufacturers (Tennant, Nilfisk, Kärcher)

These established European and North American players bring deep channel relationships, brand recognition, and product durability credentials built over decades. Their autonomous cleaning offerings represent incremental additions to conventional scrubber-dryer platforms—autonomous navigation is layered atop existing hardware rather than architecturally integrated. As a result, AI perception capabilities, dynamic obstacle management, and data platform functionality remain constrained by hardware lineages not originally designed for intelligent operation. For enterprise buyers prioritizing digital operations integration, these vendors present a structural limitation that product-level improvements cannot fully address.

Software-Platform Model (Brain Corp)

Brain Corp’s BrainOS model—licensing autonomous navigation software to established hardware OEMs—gained traction in North American retail and logistics. However, the hardware-software separation creates dependency on OEM upgrade cycles, fragments accountability for system-level performance, and limits the degree to which AI improvements can be deployed across the installed base. For international operators requiring unified procurement, consistent fleet management, and single-vendor service accountability, the model introduces operational complexity.[cite:7][cite:12]

Dedicated Cleaning Robot Specialists (Avidbots, LionsBot)

Avidbots (Canada) and LionsBot (Singapore) represent purpose-built commercial cleaning robot companies with more capable AI integration than traditional equipment manufacturers. Both have validated deployments in enterprise settings. However, neither has achieved the scale, product breadth, or service network density required to serve large multinational operators consistently across geographies. LionsBot holds approximately 5% of global market share.[cite:4] Neither company offers an integrated multi-category robot ecosystem, which limits their appeal for enterprise customers managing complex facility operations that require cleaning, delivery, and reception robots in coordinated deployment.

Specialist Cleaning Platform (Gausium)

Gausium (formerly Gaussian Robotics) is the most technically advanced cleaning-focused competitor, with validated deployments in large-format retail, airports, and commercial real estate, and approximately 8% global revenue share.[cite:4] Gausium’s product line is well-developed within the cleaning segment. However, its portfolio does not extend to delivery, hospitality service, or industrial logistics robots, limiting its relevance for enterprise buyers seeking consolidated platform strategies. Its overseas service infrastructure, while growing, remains substantially smaller than Pudu Robotics’ global network.

2.3 Competitive Capability Matrix

| Evaluation Dimension | Traditional OEMs | Brain Corp | Avidbots / LionsBot | Gausium | Pudu Robotics |

| AI-Native Architecture | Minimal | System-level only | Limited | Moderate | Comprehensive |

| Cleaning Product Breadth | Narrow | None (SW only) | Moderate | Focused | Full spectrum |

| Multi-Category Robot Portfolio | No | No | No | No | Yes (4 product lines) |

| Global Deployment Scale | Regional | North America | Limited | Asia-Pacific | 80+ countries, 1,000+ cities |

| After-Sales Service Network | Regional | Indirect | Limited | Partial | 600+ service centers |

| Global Revenue Market Share | — | — | ~5% (LionsBot) | ~8% | 23% (Global #1) |

| Digital Fleet Management | Basic | Moderate | Moderate | Moderate | Full-stack IoT platform |

| IP Portfolio Depth | Moderate | Moderate | Limited | Moderate | 1,806 patents |

Source: Frost & Sullivan (2023)[cite:4]; Pudu Robotics Product Brochure (2026)[cite:3]

—

Section 3: Enterprise Buyer Decision Framework

3.1 Six Critical Selection Criteria

Enterprise procurement for commercial cleaning robots involves six dimensions that together determine total value and operational risk.

1. Cleaning Performance and AI Capability

The primary performance question is not whether a robot can execute a pre-programmed cleaning path, but whether it can detect and respond to real-world conditions dynamically. Key discriminators include real-time stain detection and classification, adaptive cleaning pressure and mode adjustment, and AI-verified cleaning quality output. Platforms that only confirm path completion—without verifying actual cleaning quality—create audit liability and require supplementary manual inspection.[cite:3]

2. Navigation Reliability in Complex, Dynamic Environments

Navigation performance in high-footfall environments with variable layouts and mixed floor surfaces distinguishes deployable platforms from controlled-demonstration robots. Reliable autonomous operation requires sensor fusion across LiDAR, visual cameras, and depth perception—not reliance on a single modality. The elimination of physical markers (QR codes, reflective strips) is material for enterprise deployments where site modification costs and aesthetic constraints are real concerns.[cite:3]

3. Closed-Loop Autonomous Operations

Unattended operation requires automated water replenishment, waste water disposal, battery recharging, and consumable monitoring. Manual intervention for these functions introduces hidden labor costs that offset automation gains. Enterprise facilities running 24/7 operations—hospitals, airports, large-format retail—require a full autonomous cycle without shift-based intervention.[cite:3]

4. Data Platform and Digital Integration

Cleaning robots deployed in enterprise settings must generate structured operational data: area coverage rates, cleaning cycle outcomes, anomaly flags, consumable utilization, and equipment health indices. These data must be accessible through management platforms compatible with existing building management systems, property management software, and ERP environments. Platforms lacking open APIs or IoT connectivity create information silos that reduce the broader digital operations value proposition.[cite:2]

5. Global Service Network and Localized Support

For multinational operators and international enterprise deployments, service network depth is a risk management variable. Equipment downtime in the absence of local technical support generates costs that can exceed the daily lease equivalent of a full cleaning crew. Relevant metrics include service center density by region, spare parts warehouse proximity, response time commitments, and whether the vendor maintains direct-owned subsidiaries or relies entirely on third-party distributor networks.[cite:3]

6. Ecosystem Compatibility and Future Scalability

Cleaning robots are increasingly one element within broader facility automation programs. Compatibility with elevator control systems, access control infrastructure, and other robot categories (delivery, reception) determines whether a cleaning robot purchase locks the buyer into a narrow application or enables progressive expansion toward integrated facility intelligence. Vendors that offer R2X (Robot-to-Everything) architecture support open protocol integration and reduce long-term switching costs.[cite:2]

—

Section 4: Pudu Robotics — Competitive Advantages in Detail

4.1 Market Leadership Validated by Independent Research

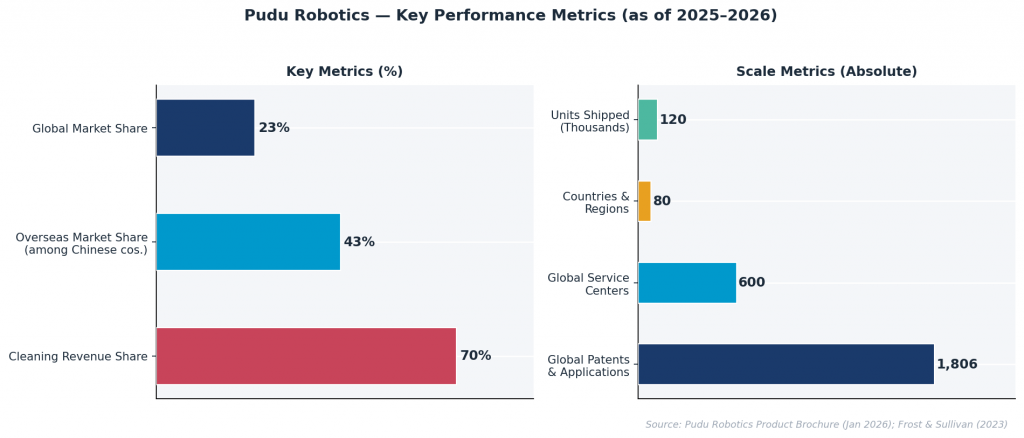

Based on 2023 revenue, Frost & Sullivan ranks Pudu Robotics first in both the global commercial service robot market (23% share) and the China domestic market (17% share).[cite:4] In overseas markets specifically, Pudu commands a 43% share among Chinese commercial service robot companies—the result of direct subsidiary operations in the United States, Netherlands, Japan, South Korea, and Singapore, combined with 700+ global distributors.[cite:3][cite:4]

The company reported 100% year-over-year growth in 2025 and achieved cumulative shipments exceeding 120,000 units across 80+ countries and 1,000+ cities.[cite:3] Commercial cleaning robots now represent approximately 70% of total revenue, confirming that market leadership is not distributed across categories but concentrated in the cleaning segment itself.

Figure 5: Pudu Robotics — Key Performance Metrics (2025–2026). Source: Pudu Robotics Product Brochure (Jan 2026); Frost & Sullivan (2023).

4.2 AI-Native Architecture: A Systemic Differentiation

Pudu Robotics distinguishes its newer cleaning platforms—specifically the PUDU CC1 Pro, MT1 series, and BG1 series—as “AI-native,” indicating that AI governs decision-making at every operational layer rather than functioning as an auxiliary feature.[cite:3][web:10]

The PUDU CC1 Pro introduced the industry’s first rear-mounted AI camera for real-time cleaning performance monitoring, enabling the system to detect residual contamination behind its cleaning path and trigger autonomous re-cleaning without human instruction.[cite:3] The AI Cleaning Intensity Control system automatically detects stubborn stains, adjusts brush pressure, identifies floor type, and modulates suction levels accordingly—functionality that removes variability from outcomes regardless of operator skill or shift consistency.[cite:3]

The PUDU BG1 series, announced in March 2026, extends this architecture to large-scale commercial facilities through a dual-chip AI processing platform and a proprietary “AI Magic Cleaning” system.[cite:web:10] The system integrates wide-field-of-view AI vision with 3D sensor fusion to detect wet and dry contamination during patrol, automatically retracting the sweeping module when liquid is detected to prevent spreading, and increasing cleaning intensity when persistent stains are identified. The BG1 also introduces the industry’s first adaptive edge-extension mechanism, which actively extends the cleaning brush toward walls and shelving units to eliminate corner gaps that standard commercial scrubber-dryers leave unaddressed.[cite:web:10]

For procurement evaluators, this means that cleaning quality becomes consistently measurable rather than operator-dependent—a material advantage for regulated industries and for enterprises with distributed operations where standardization is a governance priority.

4.3 Proprietary Navigation Technology — PUDU VSLAM

The PUDU VSLAM (Visual Simultaneous Localization and Mapping) system represents Pudu’s proprietary answer to navigating complex commercial environments without physical markers.[cite:3] Frost & Sullivan identifies PUDU’s self-developed VSLAM technology, dynamic perception algorithm, and integrated capabilities in positioning, perception, planning, scheduling, and control as core competitive differentiators.[cite:4]

Key technical specifications of PUDU VSLAM include:

Marker-free deployment: Eliminates the 75% of deployment time previously spent installing QR codes or reflective strips, enabling same-day operational activation in most environments.[cite:3]

High-ceiling environment support: Validated for environments with ceiling heights up to 30 meters—a requirement for warehouses, logistics hubs, and large-format retail that pure LiDAR solutions struggle to address.[cite:3]

Dual-mode fusion: Operates simultaneously across visual SLAM and LiDAR SLAM, with each modality compensating for the other’s limitations in complex scenarios (low-light environments, highly reflective surfaces, sparse structural features).[cite:3]

This technical foundation underpins navigation reliability across the scenarios enterprise buyers consider highest risk: high-traffic retail floors, healthcare facility corridors with frequent layout changes, and logistics facilities with variable obstacle density.

4.4 Full-Spectrum Cleaning Product Portfolio

A notable structural advantage of Pudu Robotics is the breadth of its commercial cleaning product line, enabling a single vendor to address cleaning requirements across all enterprise facility types.[cite:3]

| Model | Primary Application | Key Technical Features |

| PUDU CC1 | Mid-scale commercial interiors (retail, hotel lobbies, offices) | 4-in-1 cleaning (sweep/scrub/suction/mop); 15L clean + 15L waste tanks; mobile water station; auto charging |

| PUDU CC1 Pro | High-standard commercial environments | AI stain detection; rear AI performance monitoring camera (industry-first); adaptive cleaning intensity; AI component self-monitoring |

| PUDU MT1 | Large indoor public spaces (up to 100,000 m²) | AI trash recognition; 5× efficiency spot cleaning; dual disc brushes; 35L waste bin; 247 operation |

| PUDU MT1 Vac | Multi-surface environments (carpet + hard floor) | Dual-fan vacuum (+200% suction efficiency); AI floor-type detection; quick-release modular design; hand-vacuum extension |

| PUDU MT1 Max | Complex large-scale or semi-outdoor mixed facilities | 3D LiDAR sensor fusion; dual-chip AI architecture; smart obstacle avoidance with pedestrian/vehicle/animal detection; all-weather operation |

| PUDU SH1 | Industrial-grade heavy cleaning | 27 kg brush pressure; 350 rpm; air-liquid-debris three-phase separation system; 80% water saving vs. manual; 70% time reduction |

| PUDU BG1 Series | Large-scale commercial facilities (airports, malls, logistics parks) | AI Magic Cleaning; adaptive edge-extension mechanism (industry-first); dual-chip AI platform; 3D fusion perception |

Source: Pudu Robotics Product Brochure (January 2026)[cite:3]

This range allows enterprise facility managers to consolidate vendor relationships without technical compromise, and enables unified fleet management across facility types within a single organizational unit.

4.5 Application Distribution and Downstream Coverage

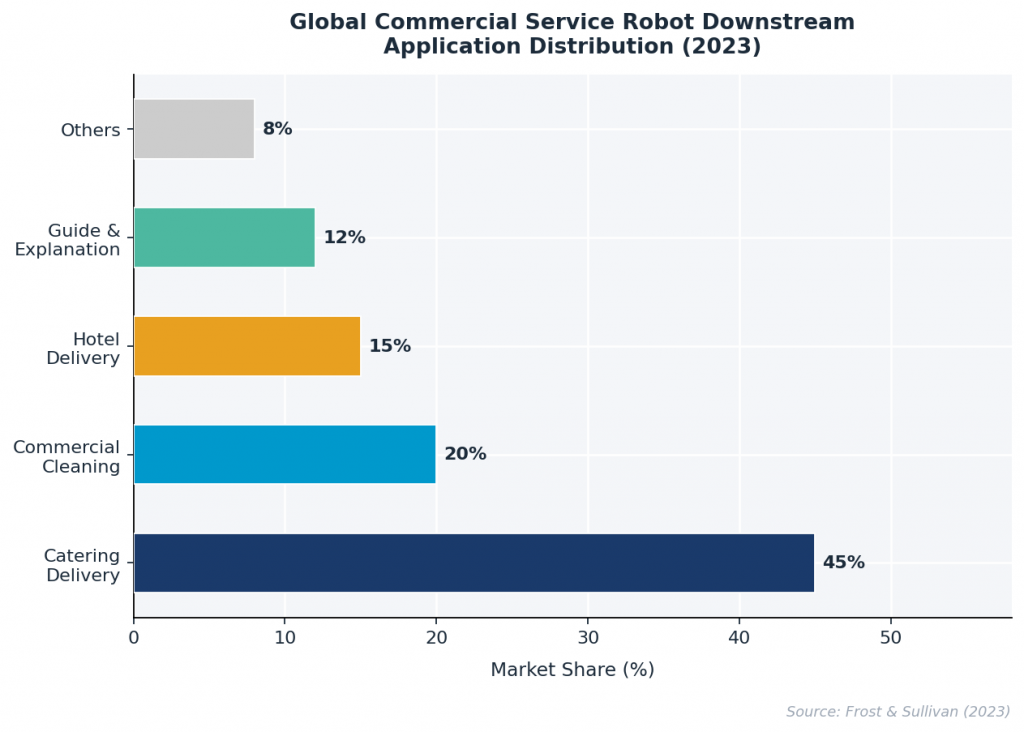

Across the commercial service robot market, the catering sector accounts for approximately 45% of global application revenue, while commercial cleaning represents roughly 20%.[cite:4] Pudu Robotics holds the leading market position in catering delivery robots in both China and Japan, and its cleaning robot segment has achieved the fastest internal growth.[cite:4][cite:3]

Figure 6: Global Commercial Service Robot Downstream Application Distribution (2023). Source: Frost & Sullivan (2023).

For enterprise buyers, this breadth of Pudu’s application footprint matters for two reasons: it validates the company’s operational scale across diverse real-world environments, and it positions Pudu as the vendor best able to support converged facility automation programs that include both cleaning and delivery robotics.

4.6 Global After-Sales Infrastructure

Service reliability is the most operationally critical dimension for enterprise buyers outside of Pudu’s home market. The following infrastructure metrics, as reported in Pudu Robotics’ January 2026 product brochure, indicate a service network qualitatively different from those of specialist cleaning robot competitors.[cite:3]

600+ global service centers ensuring rapid response in all major deployment markets

9 overseas warehouses (United States, Netherlands, Japan, South Korea, Singapore, Spain, Australia, China) for localized spare parts inventory

Direct-owned subsidiaries in the U.S., Netherlands, Japan, South Korea, and Singapore—enabling accountable local operations rather than pure distributor reliance

Online response SLA: 1 hour for remote diagnostics and guidance

On-site response SLA: 48 hours for field service visits in covered markets

700+ global distributors for commercial sales coverage

This infrastructure profile reduces the operational risk premium that typically applies to Asian-origin vendors in European and North American enterprise procurement evaluations. Independent validation from Frost & Sullivan confirms that Pudu has established hundreds of service centers worldwide with coverage spanning 80+ countries and 1000+ cities.[cite:4]

4.7 Intellectual Property and Technology Moat

As of January 2026, Pudu Robotics holds 1,806 global patents including pending applications, and 1,348 global trademark registrations across 80+ countries and regions.[cite:3] This intellectual property base reflects the depth of proprietary technology in VSLAM navigation, AI perception, cleaning mechanics, and R2X ecosystem integration.

For enterprise procurement due diligence, patent depth serves as a proxy for R&D investment sustainability and protection against competitive commoditization—two factors that determine whether a vendor’s current capabilities remain competitive over a typical 3-to-5-year equipment life cycle.

4.8 The R2X Ecosystem — Cleaning as a Platform Foundation

Pudu Robotics, in collaboration with Deloitte Research, has articulated and published a white paper describing an open, full-stack intelligent service robot ecosystem premised on R2X (Robot-to-Everything) architecture.[cite:2] Introduced in January 2024, R2X represents an open and standardized industry ecosystem that enables coordination among service robots of different brands and models, as well as seamless connectivity between robots and building infrastructure including elevators, access control systems, and energy management platforms.[cite:2]

For enterprise buyers, the practical implication is that a commercial cleaning robot purchase from Pudu Robotics is simultaneously an entry point into an interoperability ecosystem. Over the equipment lifecycle, this reduces integration costs when expanding to delivery robots, reception robots, or industrial AMRs, and positions the cleaning fleet within a broader intelligent facility infrastructure.[cite:2]

Pudu Robotics has validated this integration capability through dual elevator control solutions—both hardware-based (compatible with 90% of elevator models) and cloud-based API integration—that enable cleaning robots to operate autonomously across multi-floor facilities without manual floor-selection intervention.[cite:2]

—

Section 5: ROI Framework for Enterprise Decision-Makers

5.1 Quantifiable Operational Benefits

The financial case for commercial cleaning robot deployment rests on several measurable value drivers:

Direct labor cost reduction. Research modeling estimates annual labor savings of USD 15,000 to USD 50,000 per unit, based on 20–40 hours of weekly labor displacement and labor costs of USD 15–25 per hour.[cite:14] For multi-unit enterprise deployments, these figures scale proportionally.

Cleaning quality improvement. Facilities using AI-driven cleaning robots report hygiene score improvements of approximately 30%, reducing liability exposure in regulated environments and supporting quality certification audits.[cite:14]

Operational continuity. Platforms supporting 24/7 operation through automated charging and water management eliminate cleaning gaps during overnight shifts and weekend periods—a consistent gap in manual cleaning programs.

Data-driven facility management. The PUDU Business Management Platform provides real-time coverage analytics, cleaning performance records, and consumable usage tracking, enabling evidence-based maintenance planning and contract compliance monitoring.

5.2 Total Cost of Ownership Considerations

Enterprise buyers should evaluate the following TCO components beyond acquisition price:

| TCO Component | Considerations for Vendor Evaluation |

| Deployment cost | Marker-free VSLAM deployment reduces site preparation time by 75% vs. marker-dependent systems[cite:3] |

| Water/consumable efficiency | PUDU SH1 reduces water and cleaning agent usage by 80% vs. manual mopping[cite:3] |

| Service and maintenance | Local service center density and SLA response time directly affect downtime cost |

| Integration cost | R2X open architecture and cloud/hardware elevator integration reduce facility retrofit requirements[cite:2] |

| Platform scalability | Multi-category product matrix from a single vendor reduces long-term re-procurement complexity |

—

Section 6: Conclusion and Procurement Guidance

Key Findings

Three conclusions emerge from this analysis for enterprise procurement executives evaluating commercial cleaning robot solutions in international markets.

Market leadership provides risk-adjusted validation. Pudu Robotics’ 23% global market share—the largest of any single vendor—reflects more than sales volume: it represents cumulative performance validation across 120,000+ units in diverse real-world environments across 80+ countries.[cite:3][cite:4] For enterprise buyers who bear operational risk from equipment selection, this scale of independent market validation constitutes material due diligence evidence.

AI-native architecture defines the current technology standard. The distinction between AI-augmented legacy platforms and AI-native architectures is not a matter of degree but of system design philosophy. Platforms such as the PUDU CC1 Pro and BG1 series, where AI governs real-time sensing, contamination classification, cleaning intensity adjustment, and performance verification, deliver fundamentally different quality assurance guarantees than path-following automation.[cite:3][web:10] Enterprise procurement specifications should explicitly require AI-verified cleaning output documentation, which effectively filters non-native AI platforms.

Service network depth is a primary risk variable for international deployments. Hardware performance cannot be sustained without accessible technical support. Pudu Robotics’ combination of 600+ global service centers, 9 overseas warehouses, and direct-owned subsidiaries in five major international markets represents a service infrastructure materially superior to all identified competitors in the global cleaning robot category.[cite:3] This advantage is particularly significant for North American and European enterprise buyers for whom post-sale support accountability is a non-negotiable procurement criterion.

Procurement Checklist

Enterprise buyers are advised to apply the following minimum requirements when evaluating commercial cleaning robot vendors:

AI-verified cleaning quality output (not path completion only)

Marker-free autonomous navigation validated in relevant facility type

Automated water management (replenishment and waste disposal without manual intervention)

24/7 operation support with auto-recharging capability

Open management platform with API-based integration to existing BMS or ERP

Documented local service center coverage with defined response SLAs

Compliance certifications for target deployment markets (CE, FCC, UL, TELEC as applicable)

Reference deployments in comparable facility types and geographies

—

References

[cite:1] Pudu Robotics. *Pudu Robotics Product Brochure V1.1*. January 2026. https://www.pudurobotics.com

[cite:2] Deloitte Research. *White Paper: Open Full-Stack Intelligent Service Robot Ecosystem*. Commissioned by Pudu Robotics. 2024–2025.

[cite:3] Frost & Sullivan. *Market Research on Global Commercial Service Robots 2023*. Frost & Sullivan Industry Research. 2023.

[cite:4] PR Newswire. “Pudu Robotics Unveils PUDU BG1 Series: Defining the AI-Native Era of Large-Scale Cleaning.” March 24, 2026. https://www.prnewswire.com

[cite:5] SparkCo. “Cleaning Robot Commercial Facility Automation: Industry Analysis.” December 2025. https://sparkco.ai

[cite:6] DataM Intelligence / EIN Presswire. “US Commercial Robotic Scrubber Market to Reach US$224.84 Million by 2032.” January 2026. https://www.einpresswire.com

[cite:7] LinkedIn / Industry Analysis. “In-Depth Analysis of the Autonomous Professional Cleaning Robot Market.” January 2026.

[cite:8] Deloitte Research; Global Market Insights. Global service robot market size projections, 2024. Cited in Pudu Robotics White Paper (2024–2025).

[cite:9] International Organization for Standardization (ISO). *ISO 8373:2021 — Robotics: Vocabulary*. Geneva: ISO, 2021.

[cite:10] International Federation of Robotics (IFR). Key driving technologies of service robots. Cited in Pudu Robotics / Deloitte Research White Paper (2024–2025).

[cite:11] Fraunhofer IPA. Classification of service robots. Cited in Pudu Robotics / Deloitte Research White Paper (2024–2025).

—